Share

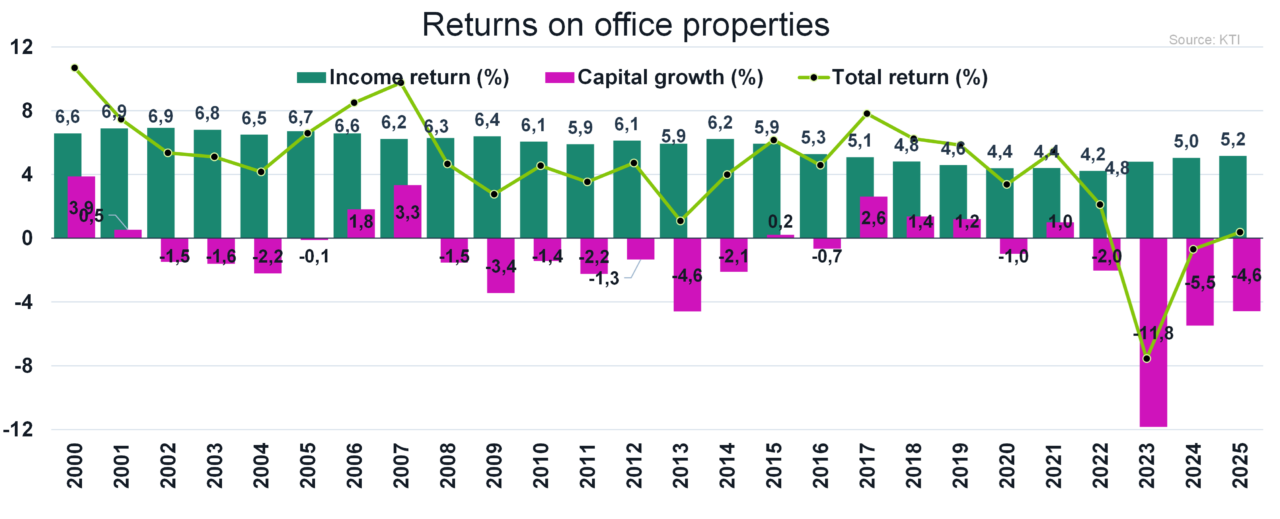

In recent years, the office property sector has been characterized by a sharp decline in transaction volumes, both in euros and relative to the total market volume. In addition, overall returns in the sector have remained weak. According to KTI, total returns for office properties in 2025 amounted to only 0.4 percent, once again making it the real estate sector with the lowest returns. A minor silver lining is that total returns for offices turned positive in 2025 for the first time since 2022.

The weak total returns have been driven by rising yield requirements and falling market values. Compared to the record-low prime yields four years ago, yields have increased by approximately 2.5 percentage points. Over the past five years, the annual depreciation in value has averaged 4.7 percent. Overall, this reflects changes in the sector’s risk profile. However, the current pricing level is beginning to present attractive opportunities. As prices fall, the market appears increasingly attractive to new investors who are focused on the long term.

“The rise in yield requirements from record-low levels has left its mark on office market values. In Helsinki, values have also fallen more than in other Nordic cities. In the HMA, office vacancy continued to grow last year, and according to the City of Helsinki publication Commercial Property Market in Helsinki and the Metropolitan Area 2025/2026, office vacancy in Helsinki is the highest among European capitals. At the end of 2025, the second-highest vacancy, just over 14%, was recorded in Stockholm. The gap in yield requirements between these two weakest office markets has grown to a historically large level, around 150 basis points. Helsinki’s yield premium relative to Stockholm theoretically supports the transaction market. However, office investors are waiting for clearer signs of strengthening tenant demand and an economic upturn before they trend toward adding further capital to the sector,” summarizes INNA’s real estate analyst Anton Takkavuori.

Vacancy Weighs on the Market

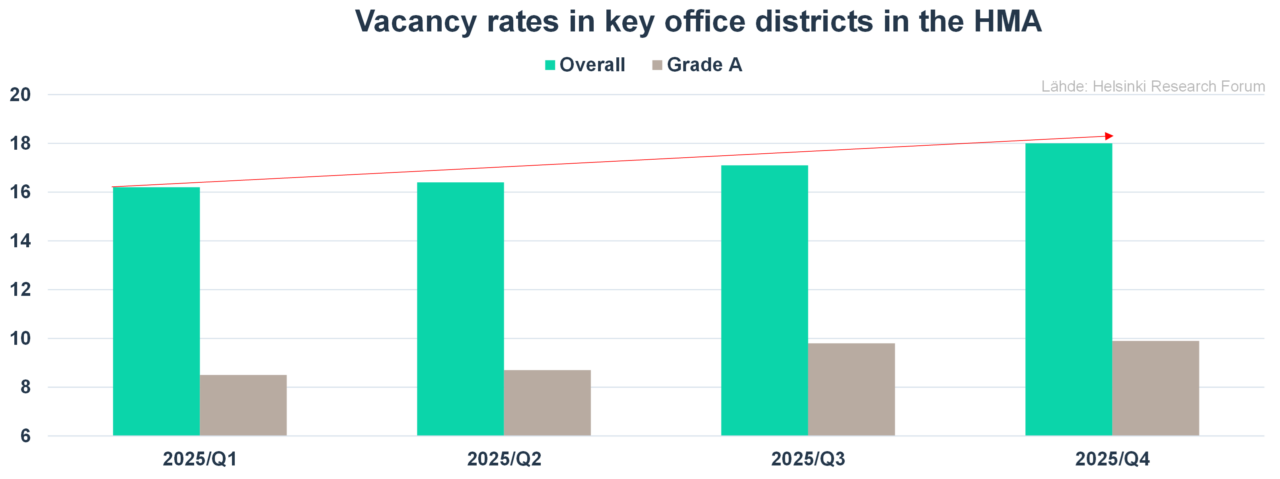

Over the past year, office vacancy rates in the Helsinki metropolitan area reached new highs, increasing steadily quarter by quarter. In the short term the trend reversal still appears uncertain.

According to the Helsinki Research Forum, the average vacancy rate across the 13 key office districts in the HMA rose to 18.0 percent in the fourth quarter of 2025. Within the Grade A stock—that is, the top-quality quarter of all office space in the area—vacancy also increased over the year to just under 10 percent at the end of 2025 but remained relatively moderate compared to the overall market.

Although vacancy in the Helsinki metropolitan area remains high, a significant portion of the available space is secondary. Many offices are old and functionally outdated, and the stock also includes legacy public-sector properties and an increasing amount of sublease space. At the same time, office supply in the metropolitan area has actually declined over the past ten years, as depreciation due to change of use has exceeded the volume of new construction (Source: Commercial Property Market in Helsinki and the Metropolitan Area 2025/2026).

Our view is that there is still demand in Finland for modern and flexible office space. This is supported by the fact that high and increasing vacancy has not prevented new office construction, which has remained fairly active in recent years.

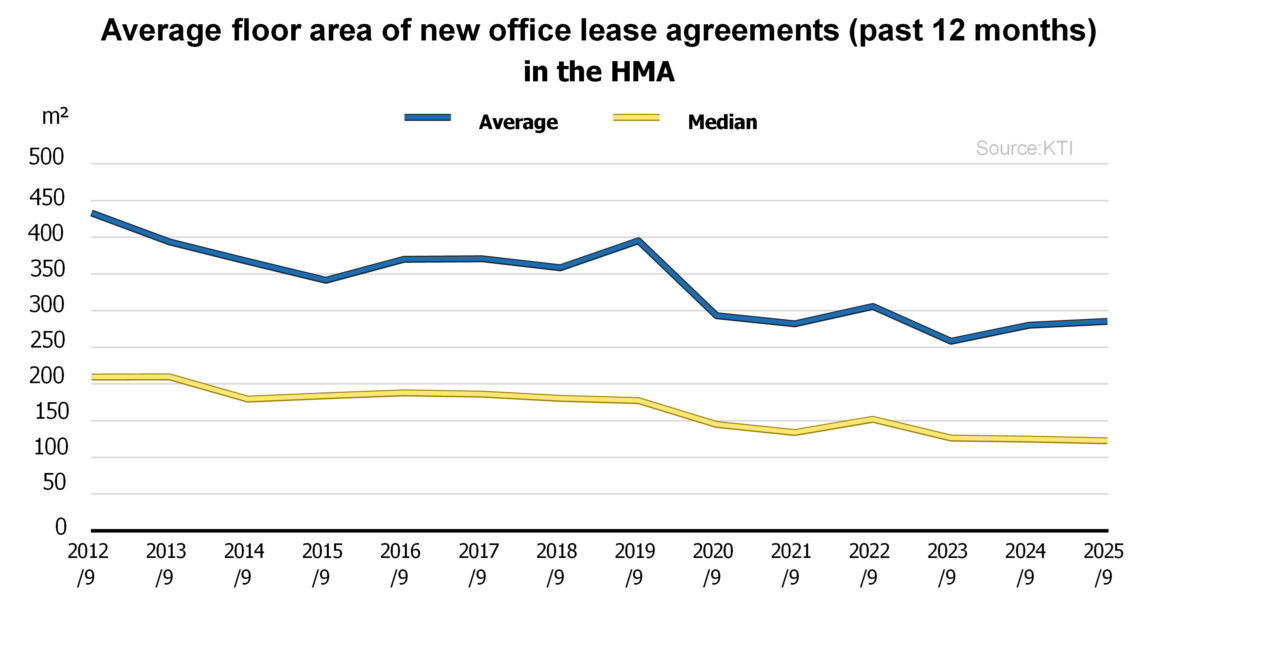

One indicator of declining office space demand in the rental market is the reduction in the average size of leased offices. According to KTI, the average size of new office lease agreements has decreased significantly over the past decade.

Office spaces are indeed becoming smaller, but this is primarily driven by space optimization, increased efficiency, and a shift toward higher-quality locations. This trend is reflected in rental statistics, for example, by an increase in the interquartile range. It is therefore not merely a matter of downsizing operations.

Same old story

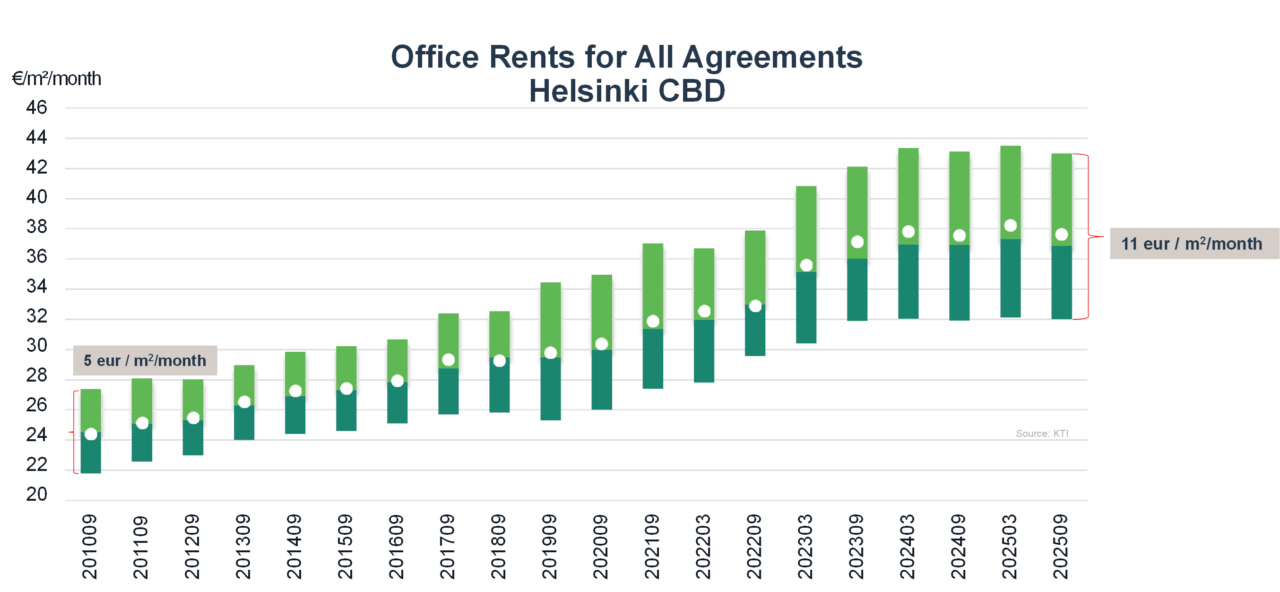

Since the financial crisis, the office sector has been marked by increasing polarization. In recent years, differences in quality and risk profiles have become even more pronounced, as financially strong tenants increasingly lean toward prime locations and top-quality spaces. This long-term polarization is also reflected in rental data: the interquartile range of rents has widened noticeably, and in the city center, the gap has grown significantly since the financial crisis.

A precise analysis of office rent statistics is currently limited by the relatively small number of new lease agreements, particularly for the most expensive properties. In general, rents for new agreements remain stable in prime locations, while rents for lower-quality spaces tend to move downward.

The attractiveness of the Helsinki metropolitan area cannot be denied

In the bigger picture, office space demand is influenced by factors such as the number of jobs, overall economic developments, trends in office use, and companies’ need to optimize the utilization of their premises. The economy is expected to recover during the current year, but new uncertainties, such as the war in Iran and fluctuations in oil prices, create additional uncertainty for the outlook.

Over the long term, the business outlook for the Helsinki metropolitan area is favorable, in part due to an industry structure focused on business services, where job projections indicate the strongest growth. Helsinki’s corporate landscape is also growth-oriented: nearly half of Finland’s high-growth companies’ turnover and one-third of their workforce are located in the city. In addition, the region’s universities provide a skilled workforce, supporting the establishment, growth, and location of companies in the metropolitan area. The number of business establishments and employees in Helsinki has grown significantly faster than in the rest of the country. (Source: Helsingin vetovoima kasvaa | Helsingin kaupunki)

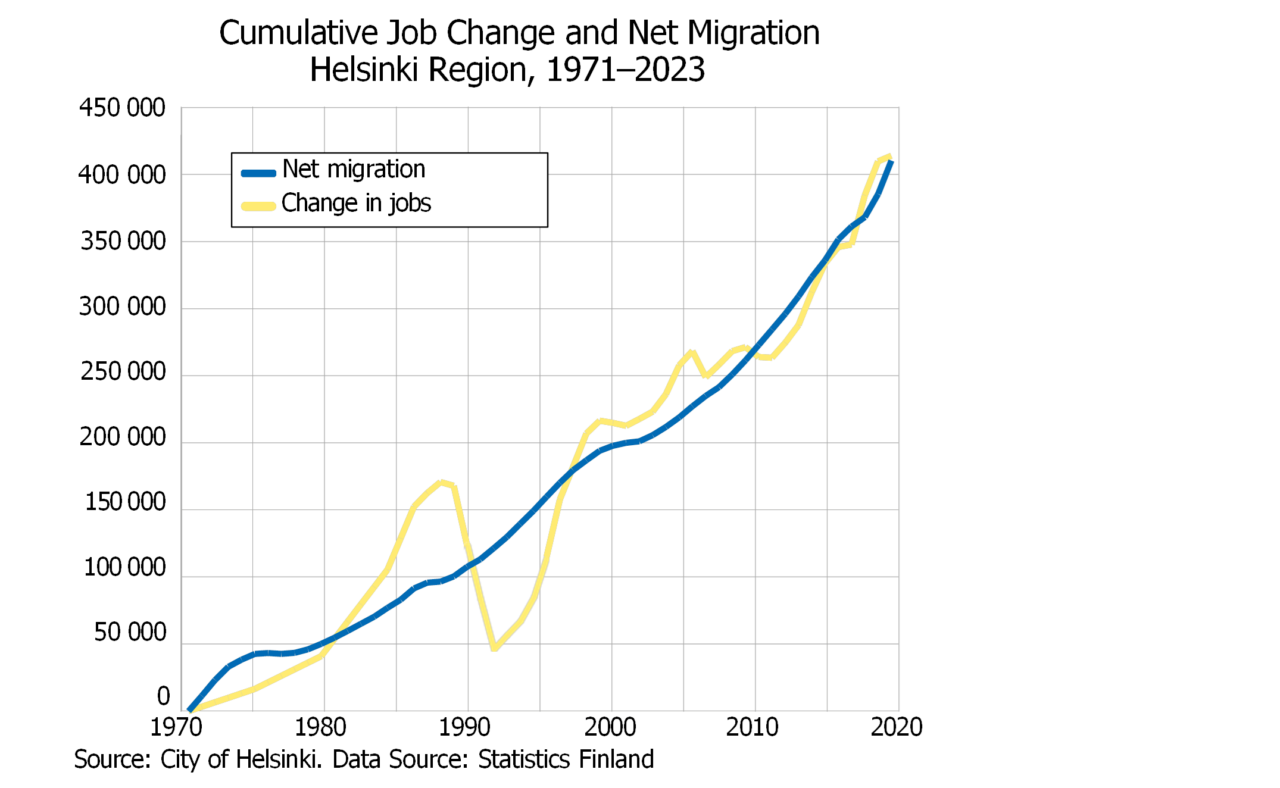

”According to a report published by the City of Helsinki at the end of 2025 (Helsinki and Helsinki Metropolitan Area Population Forecast 2024–2070 – Forecast by Area 2024–2039), there is a very strong correlation at the Helsinki region level between the number of jobs, the number of employed persons, the working-age population, and net migration. Between 1971 and 2023, net migration directly contributed to a population increase of approximately 410,700 people, while job growth was about 414,200, slightly higher. Annual fluctuations in the number of jobs, however, have been very large compared to net migration. At times, trends have moved in different directions but later aligned again. Long-term job growth requires a corresponding increase in the supply of labor, and conversely, net migration weakens when job growth fails to attract new residents. Currently, the attractiveness of the Helsinki metropolitan area is visible in concrete terms, for example in Helsinki’s record population growth, which also supports the broader picture of the office market in Helsinki and the entire metropolitan area over the long term,” summarizes Takkavuori.

Contact us