Share

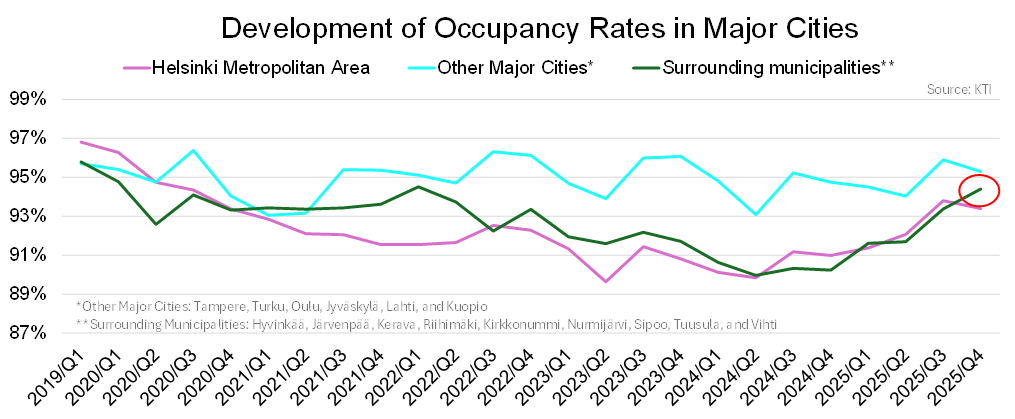

After the autumn, the rental market has remained fairly stable in major cities. Both immigration and intermunicipal net migration migration typically peak annually in Q3. During the winter months, migration slows down, which was reflected in a decline in occupancy rates in Q4. According to KTI, occupancy rates decreased in Q4 compared to Q3 in both the Helsinki Metropolitan Area (HMA) and in other major cities overall. In the HMA, the decline was concentrated in Vantaa, while in Helsinki and Espoo occupancy remained stable at around 94%.

In major cities outside the HMA, occupancy rates in Q4 ranged from 94.4% in Turku to 96.5% in Kuopio. Although occupancy rates remained relatively high in some cities, market-based rents declined in all major cities – including those where occupancy levels were strong. This underscores the fact that rent development is not driven solely by the volume of supply. Changes in tenants’ purchasing power also play an important role.

“After Q3, the development of occupancy rates among professional investors has relied largely on landlords’ own measures, as Q4 is seasonally a quieter period in terms of rental demand. However, some exceptions were also seen towards the end of the year. In the municipalities surrounding the Helsinki Metropolitan Area, occupancy rates have continued their steady increase, and in Q4 they exceeded the level of the HMA, approaching the average level of other major cities. In addition to migration flows, the rental market in these surrounding municipalities is supported by lower unemployment compared to the HMA which improves tenants’ purchasing power and reduces risks for landlords. Combined with rising occupancy rates, this strengthens the attractiveness of the surrounding municipalities from an investor perspective,” summarizes INNA’s real estate analyst Anton Takkavuori.

On the Difficulty of Forecasting

Although occupancy rates in major cities declined towards the end of the year, by Q4 2025 they had already clearly recovered from their lowest levels. This development reduces investors’ risk and indicates a gradual stabilization of the market. At the same time, demand for rental apartments is expected to grow in major cities during the current year as the number of households increases.

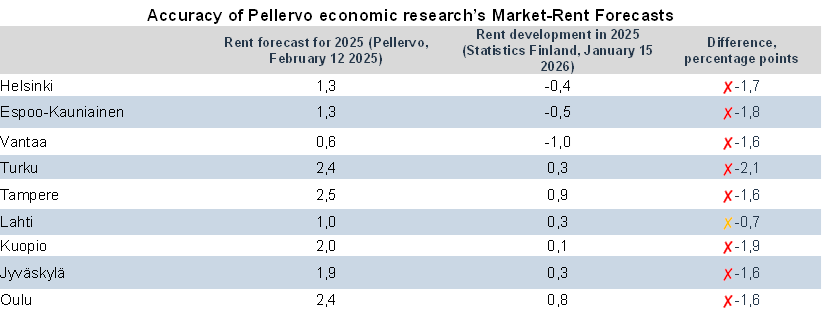

In the medium term, upward pressure on rents is anticipated as the current oversupply gradually absorbs from the market. In the short term, however, the outlook remains uncertain. This is illustrated by rent forecasts, which in recent years have tended to exceed actual developments.

In early 2025, Pellervo Economic Research PTT predicted that rent growth in the HMA would accelerate due to increasing housing demand. However, the accuracy of these forecasts proved limited, as rent developments were way weaker than expected. Although fundamentals suggest positive rent growth over the longer term, short-term predictability remains low.

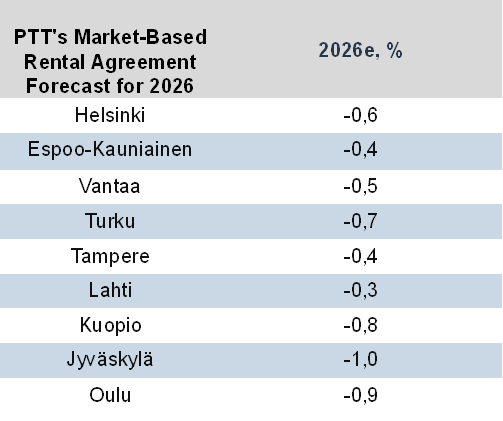

In its latest forecast, published on February 12, 2026, PTT expects rent growth in early 2026 to remain subdued, but anticipates a moderate increase towards the end of the year. According to PTT’s forecast, the annual average would still fall below last year’s level.

According to PTT, the rental market in major cities currently depends on the overall economy picking up. The main things needed for rents to keep rising are stronger economic growth, better employment, and renewed consumer confidence.

Consumer Conditions Still Temper Short-Term Expectations

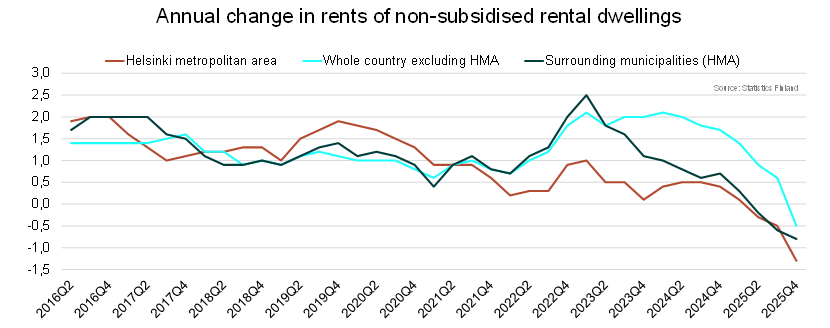

In Q4, market-based rents fell in all ten largest cities compared to the same period last year, according to Statistics Finland. Rent declines were also observed in areas where occupancy rates remain high. One key explanation is the weakening of subsidies. In addition, rising living costs and a deteriorating employment situation have increasingly affected tenants’ ability to pay. These factors partly explain the current decline in rents.

In an environment of declining rents, landlords’ need to retain good tenants becomes more pronounced. Finding a new tenant may no longer be statistically feasible at the same rent level, making efforts to improve tenant satisfaction justified in investors’ portfolios.

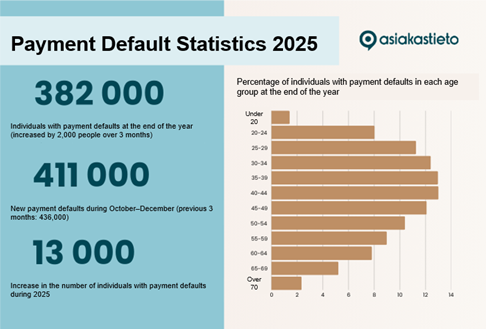

The deepening of households’ financial difficulties is reflected in the trend in evictions: the annual number of evictions remained relatively stable from 2015 to 2021, but since 2022 eviction numbers have clearly increased. The most common reason for evictions is unpaid rent.

According to Suomen Asiakastieto Oy, the total number of consumers with payment defaults continued to grow last year, although the growth rate slowed by nearly 30 percent, suggesting that the worst acceleration phase may be behind us. The company estimates that a potential improvement in employment could slow the growth rate of payment defaults this year.

Residential Real Estate Investment Market Gains Momentum

The investment market always looks ahead. Strengthened interest from international investors in Finland supports a positive market outlook. According to KTI, the growth in total transaction volume in 2025 was driven precisely by a recovery in foreign investment demand: the share of international investors in the total annual transaction volume rose to 60 percent, and they acquired properties in Finland for approximately €2.6 billion, compared with around €1 billion in the previous year. The most significant portfolio transactions in Q1 2026 have included Storebrand’s acquisition of 999 apartments from Ilmarinen (Inderes estimate: EUR 180–200 million) and Varma’s sale of a portfolio of 4,761 apartments to the listed company Kojamo (approximately EUR 900 million). These transactions support the view that the EUR 950 million transaction volume in residential portfolios recorded in 2025 (source: KTI) will be clearly exceeded in 2026.

“Liquidity in large residential portfolios has clearly improved, reflecting investors’ confidence in the rental markets of the growth triangle, despite short-term uncertainties. A concrete sign of increased liquidity is OP’s decision to reopen its real estate funds for redemptions after the year-end closure. Improved liquidity is also supported by the stabilization of valuation levels: according to KTI’s 2025 Special Investment Fund Review, property values stabilized in H2 2025, with an average change in value of 0.0 percent. On the whole, value stabilization creates conditions for the next phase of recovery in the transaction market,” summarizes Takkavuori.

Sources: KTI, PTT and Statistics Finland

Additional information:

Anton Takkavuori

Real Estate Analyst

INNA

anton.takkavuori@inna.fi

0400 853 528