Share

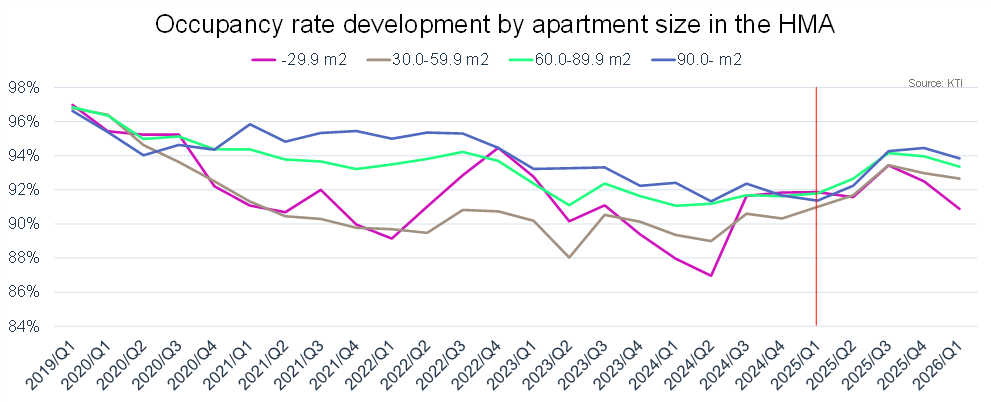

The number of completed dwellings has still exceeded the growth in housing demand in Finland’s growth triangle, according to Nordea. The subsidised housing construction has supported overall supply, while cuts to housing benefits and a weak economic have led households to live more densely. For example, population growth in the HMA was 2.8 times higher than the increase in the number of households last year. In the HMA, the occupancy rate of rental apartments fell to 92.9% in Q1’26, according to KTI, down 0.5 percentage points from Q4’25.

Over the past two years, average household size has started to increase after a long decline. This shift in housing trends is visible in the market. In Q1’26, the occupancy rate in the HMA was approximately 1.5 percentage points higher than a year earlier. The increase is mainly driven by larger rental apartments. In units over 90 m², occupancy rates rose by 2.5 percentage points year-on-year, while the 30–89.9 m² segment also saw a solid increase. The exception is apartments under 30 m², where occupancy rates in the HMA declined by one percentage point from a year earlier.

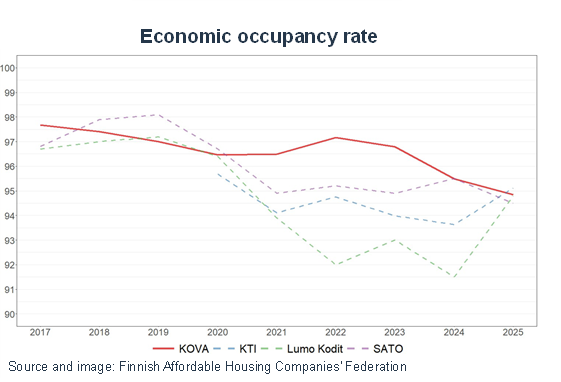

“In recent years, rents—particularly in the Helsinki Metropolitan Area—have largely stagnated despite inflation. At the same time, a turnaround in occupancy rates has already been observed in favour of institutional investors, even though interest-subsidised ARA construction has continued to support housing supply despite the collapse in free-market development. The significant volume of subsidised housing production has slowed the rebalancing of the rental market, as ARA properties compete in part for the same tenants as non-subsidised rental apartments. To reduce vacancy, institutional investors have adopted dynamic pricing strategies, which have supported improvements in occupancy rates. In contrast, occupancy rates in ARA properties have declined. This is reflected in KOVA (Finnish Affordable Housing Companies’ Federation) member organisations’ average occupancy rate, which fell to 94.8% last year. In a market with abundant supply, dynamic pricing has become a key tool enabling professional investors to improve occupancy and adapt to changing market conditions”, summarizes INNA’s real estate analyst Anton Takkavuori.

Economic conditions reflected in evictions

Alongside abundant supply, rents are also affected by a weakening economic environment: cuts to housing benefits and general economic uncertainty have led households to live more densely, reducing housing demand. The economic situation is also reflected in the day-to-day operations of professional landlords through eviction cases. The payment defaults highlighted in our previous quarterly review were, as expected, also visible in new eviction statistics.

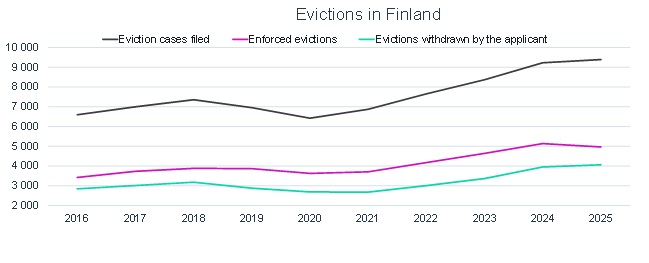

According to the National Enforcement Authority Finland’s statistics, the number of evictions has increased annually since the post-pandemic years. Last year, the trend already appeared to be levelling off, but developments towards the end of the year pushed the figure to a new record. On a positive note, the National Enforcement Authority Finland reports that in an increasing number of cases, eviction applications were withdrawn as tenants moved out voluntarily.

The number of eviction cases increased by 1.8% in 2025 compared to the previous year, with nearly 9,400 cases filed. The number of enforced evictions, however, declined by almost 3.4% from 2024, to just under 5,000.

Cases where landlords withdrew eviction proceedings rose by 2.8% year-on-year to just over 4,000. Overall, however, eviction levels remain elevated. The most common reason for eviction is rent arrears.

The Via Dolorosa of Housing Construction

Interest-subsidised ARA construction has supported housing supply despite a sharp decline in free-market development. According to Nordea, the share of subsidised housing production in Helsinki, for example, rose to as much as 70% last year. Significant cuts to ARA authorisations in the current and coming years, as well as the phasing out of HITAS (regulation system for the price and quality level of dwellings built on rented plots owned by the City of Helsinki) and right-of-occupancy support schemes, will clearly reduce subsidised housing production in the years ahead, in turn creating room for a recovery in private construction. At present, the construction of new rental housing is already declining significantly, including in the HMA, as subsidised ARA construction is reduced—gradually tightening supply over time.

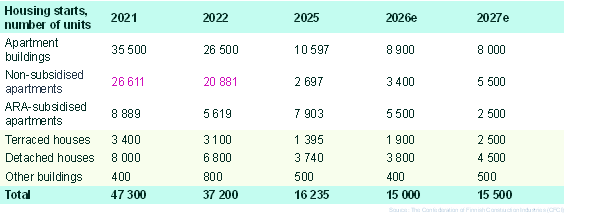

The Confederation of Finnish Construction Industries (CFCI) has significantly revised down its forecast for housing starts this year. Housing construction is now expected to decline by 3%, compared with an earlier projection of a 12% increase for 2026. The number of starts is forecast to fall to around 15,000 units (2025: 16,200), down from a previous estimate of roughly 20,000. According to CFCI, the risk of weaker-than-expected development remains substantial. Overall, housing production has fallen to levels last seen in the 1950s, which CFCI considers insufficient to meet the needs of urbanisation. This year will mark the fourth consecutive year in which housing production remains clearly below 20,000 units.

The downward revision in housing construction forecasts is explained almost entirely by weaker-than-expected developments in non-subsidised apartment construction. CFCI now estimates that starts of non-subsidised apartments will fall to around 3,400 units in 2026, compared with a previous forecast of as many as 9,000 units. During the peak years of housing construction, a large number of non-subsidised rental apartments were built, particularly by funds, driven by strong demand. These investors were key financiers and developers of new rental housing projects, and their withdrawal from the market has left a clear gap.

After the storm comes calm

Residential property values declined significantly between 2022 and 2024. Although value changes in KTI’s Property Index remained slightly negative in 2025, they were already close to zero. In Helsinki and Tampere, values even turned marginally positive.

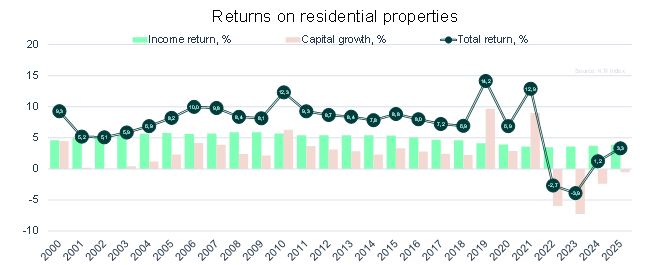

Total return on residential real estate rose to 3.3% (2024: 1.2%). The level remains low compared with the long-term average of around 7.2% over the past 20 years. However, last year’s result was the strongest for residential portfolios since 2021, when total returns stood at 12.9%. Despite the still subdued return level, the gradual market recovery has supported improving investor sentiment.

“Before the pandemic, occupancy rates among institutional investors were at around 97%. Against this backdrop, recent years have been quite exceptional in the rental market, also in terms of returns. Historically in Finland, direct residential real estate investments have delivered competitive total returns even compared with equity markets, but a key advantage of residential portfolios has been their low return volatility. According to Nordea’s assessment, if average household size remains unchanged and net migration continues to be strong, oversupply could start to unwind as early as 2027, which would also improve the operating environment for residential investors. The gradual improvement in the rental market is already reflected in the residential portfolio transaction market through increased activity”, summarizes Takkavuori.

Anton Takkavuori

Real Estate Analyst

INNA

anton.takkavuori@inna.fi

0400 853 528